•

Broadly interest rate cycles

have peaked both in India and

globally.

• Investors should add duration

with every rise in yields.

•

Mix of 10-year duration and

2-4-year duration assets are

best strategies to invest in the

current macro environment.

•

Credits continue to remain

attractive from a risk reward

perspective give the improving

macro fundamentals.

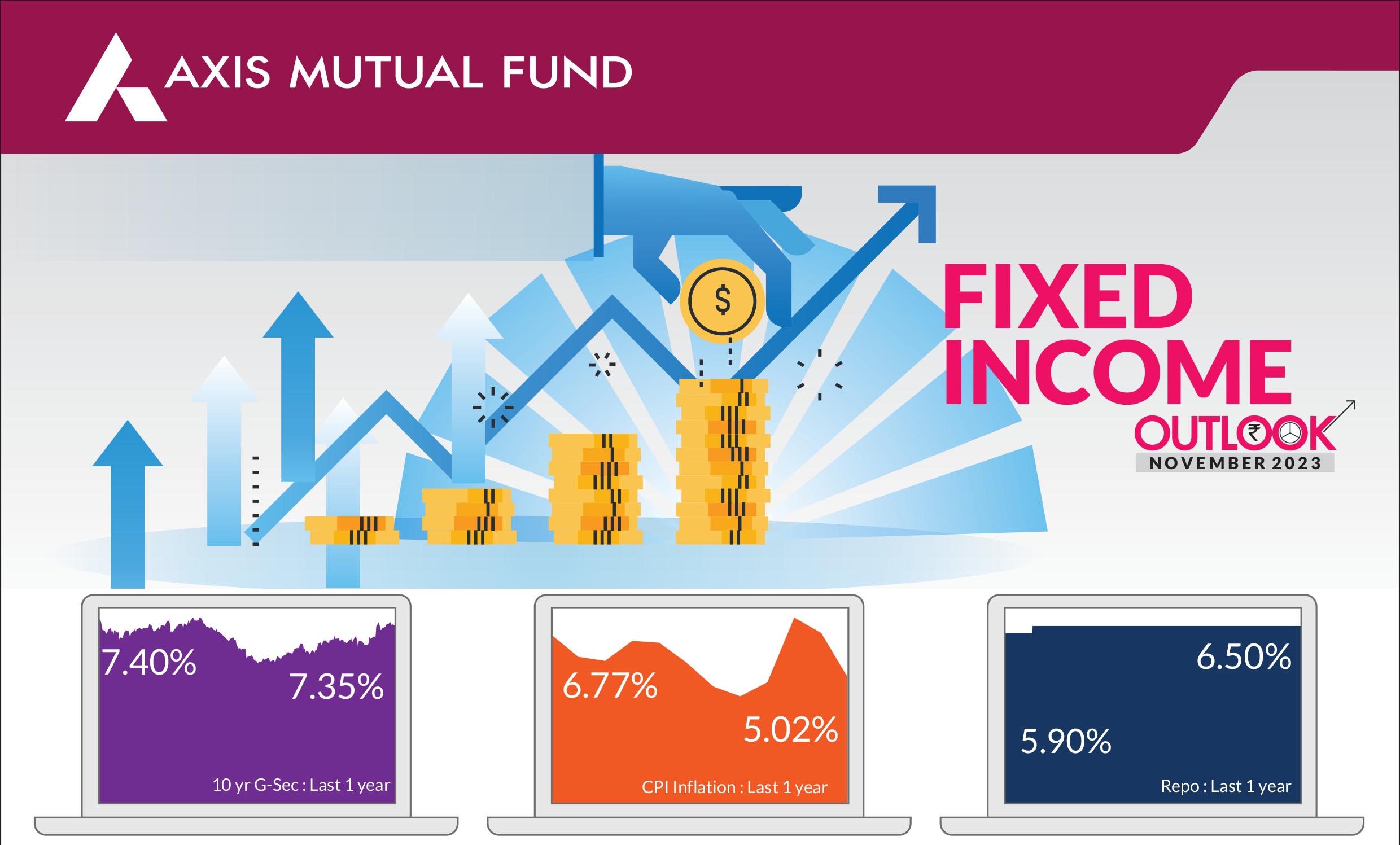

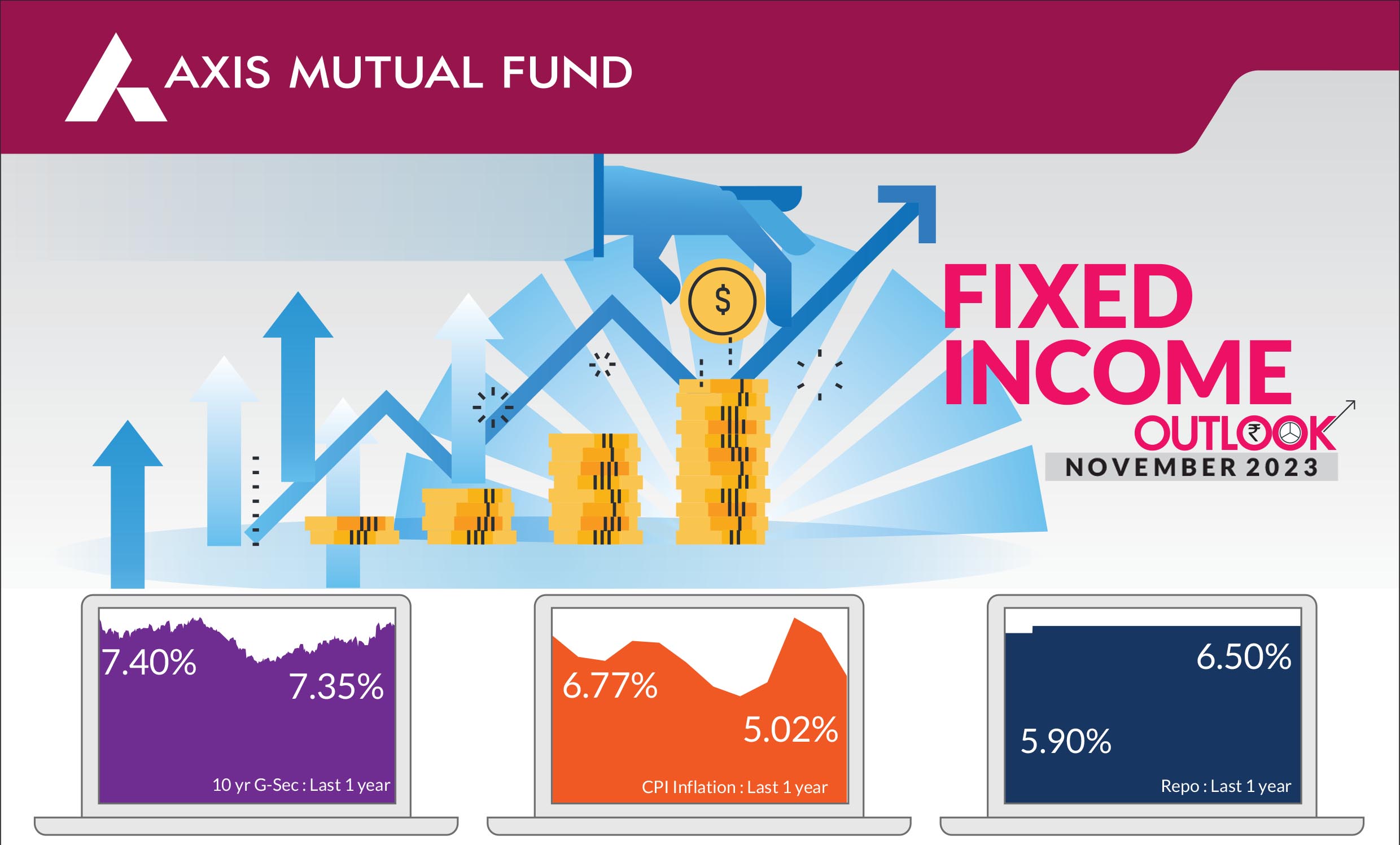

Indian government bond yields rose higher over the month, trading in a wider band of 7.23-7.40%. The key factors driving the bond markets were the rising US Treasury yields, the geopolitical conflict between Israel and Hamas, and the likelihood of OMO sales by the Reserve Bank of India (RBI). Debt markets witnessed higher inflows over the month due to the higher yields offered by Indian government bonds. The impending inclusion of government bonds in JP Morgan Global Indices has also evinced interests from FPIs.

► US Treasury yields rise over the

month, growth defies slowdown

fears:

The yields on the 10-year US

Treasury briefly touched 5%

before falling to 4.85-4.95% levels.

Fiscal deficit in the US rose to

~$1.7 trn for the year ended

September 2023 and this could likely keep yields elevated. The US economy

resisted fears of an impending slowdown and posted stronger than expected

growth. The country's GDP expanded 4.5% in Q3FY24 vs 2.1% in the

previous quarter due to a tight jobs market and higher consumer spending. In

a widely expected move, the Fed held the federal funds rate unchanged for

the second consecutive month in a target range between 5.25%-5.5%. The

Fed chairman Jerome Powell said that the process of bringing down inflation

to 2% has a long way to go and they will remain data dependent. However, we

believe tighter financial conditions and higher treasury yields have resulted

into an indirect rate hike.

► Inflationary pressures dissipate while oil prices also fall:

Headline inflation

further moderated to 5.02% as against 6.8% seen in August following a broad

based decline in vegetable prices. Core inflation, too retreated to 4.6% vs

4.8% in August. While inflation is within the central bank's band of 2-6%, the

governor has emphasized that they are targeting the 4% midpoint thereby

signaling no change to their stance on the monetary policy. However, the

below average monsoon could keep prices elevated, particularly for cereals

and pulses. Surprisingly, crude oil prices fell to below $90 even amid

increasing fears of the conflict in West Asia intensifying further.

► Central banks remain on a pause: Central banks of the large developed economies are now on a pause mode. This includes the key ones, the US, Europe and the UK. "Higher for longer" theme prevails across economies. The focus has moved from how high interest rates can go up to how long will interest rates stay elevated. The RBI in its monetary policy meeting in early October held interest rates unchanged but surprised the markets with unexpected Open Market Operations (OMOs). The minutes of the meeting released later in the month outline the MPC's unanimous views on the transient spike in headline inflation, along with moderating core inflation, keeping policy rates steady and anchoring of inflationary expectations. On the growth front, all members were concurrent on the resilient trend in growth, driven by broad-based strength in domestic demand, notwithstanding weak global growth and uncertain macro environment.

► Central banks remain on a pause: Central banks of the large developed economies are now on a pause mode. This includes the key ones, the US, Europe and the UK. "Higher for longer" theme prevails across economies. The focus has moved from how high interest rates can go up to how long will interest rates stay elevated. The RBI in its monetary policy meeting in early October held interest rates unchanged but surprised the markets with unexpected Open Market Operations (OMOs). The minutes of the meeting released later in the month outline the MPC's unanimous views on the transient spike in headline inflation, along with moderating core inflation, keeping policy rates steady and anchoring of inflationary expectations. On the growth front, all members were concurrent on the resilient trend in growth, driven by broad-based strength in domestic demand, notwithstanding weak global growth and uncertain macro environment.

Market view

US Treasury yields briefly breached the 5% mark before retreating to 4.93% at end of October and 4.75% post the policy announcement. We expect the yields to trade in a higher range. Concurrent to our view, the Fed held interest rates unchanged and we believe that the top has already been reached. The US economy did exhibit strong growth contrary to market expectations, and the macro data also has been robust - a strong payrolls report, and rising retail sales. However, we still hold our view that growth has probably peaked and slowdown could become more apparent in the coming quarters. Our view is based on two reasons - slowdown in China that will have repercussions globally and "higher for longer rates" in the developed economies. Central banks will remain on hold until inflation sustains at lower levels and based on the strength of the economy. The struggle in US is becoming increasingly apparent through rising credit card defaults, higher number of corporate bankruptcy filings and the higher fiscal deficit. Likewise, the central banks too have reached a peak of their rate cycle and we expect growth to be subdued in these economies as well. Policy makers in China are trying to boost the economy with modest support for the property sector, infrastructure spending and consumption. However we believe these would have a limited impact in turning around the economy.In India, headline inflation declined and is within RBI's comfort zone. While the central bank expects it to fall further, the effects of imported inflation (crude oil prices) and a deficit monsoon could set the momentum. Briefly, we could again see rising vegetable prices resulting into higher price pressures but we do not expect these to be a grave concern. We believe that the RBI will remain on a pause mode till the first half of 2024 and will make use of liquidity management tools to navigate any uncertainties emanating globally. The likely inclusion of government bonds in Bloomberg indices could further boost inflows. Most part of the fixed income curve is pricing in no cuts for the next one year. We reiterate that interest rates have peaked globally and in India. With policy rates remaining incrementally stable, we have added duration gradually across our portfolios within the respective scheme mandates. We do expect the 10-year bond yields to touch 6.75% by April - June 2024.

From a strategy perspective, we continue to add duration across portfolios within the respective investment mandates. We expect our duration call to add value in the medium term. Investors could use this opportunity to top up on duration products with a structural allocation to short and medium duration funds and a tactical play on GILT funds.

Source: Bloomberg, Axis MF Research.