•

Broadly interest rate cycle and

inflation cycle have peaked

both in India and globally.

• Investors should add duration

with every rise in yields.

•

Mix of 10-year duration and

2-4-year duration assets are

best strategies to invest in the

current macro environment.

•

Credits continue to remain

attractive from a risk reward

perspective give the improving

macro fundamentals.

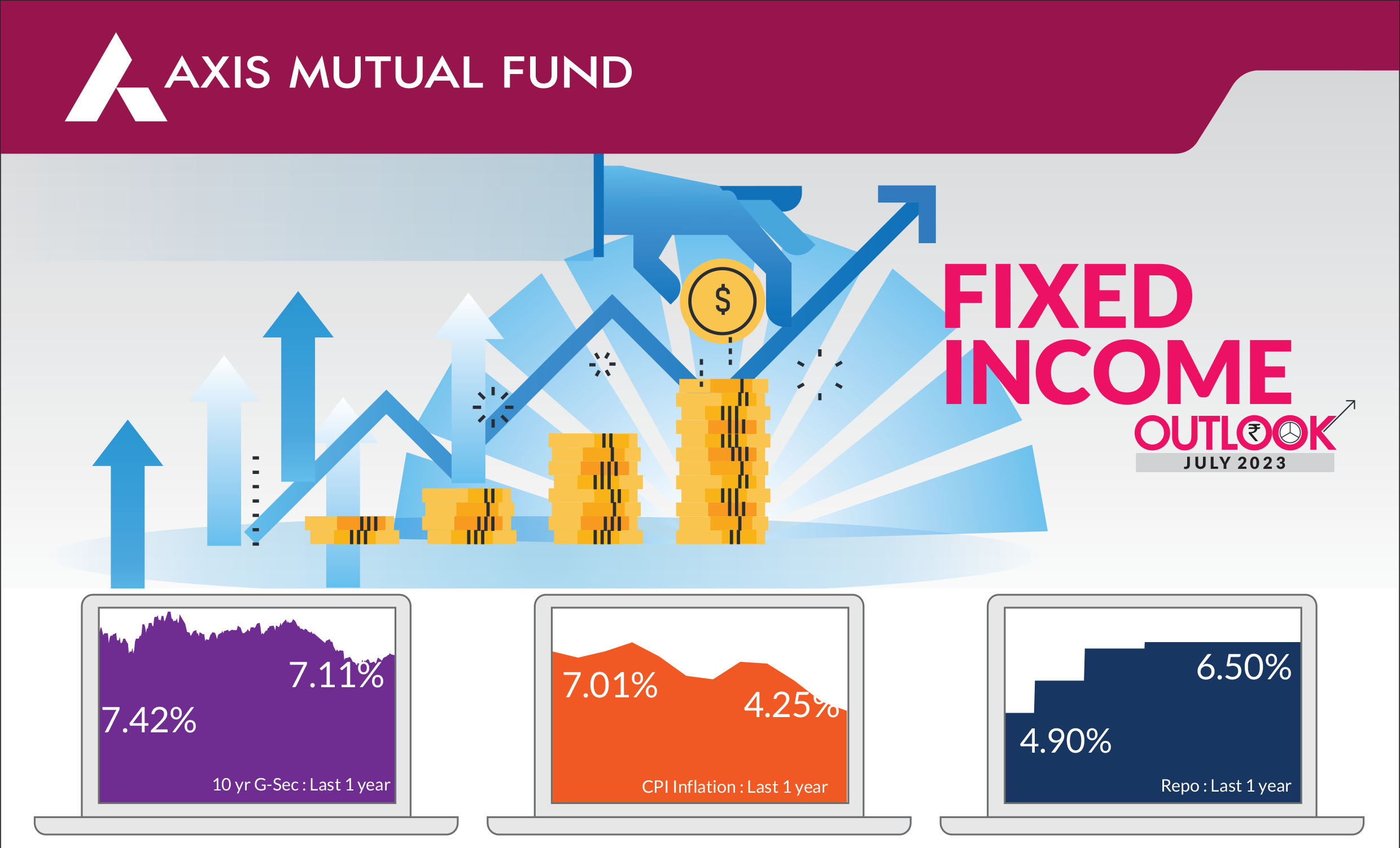

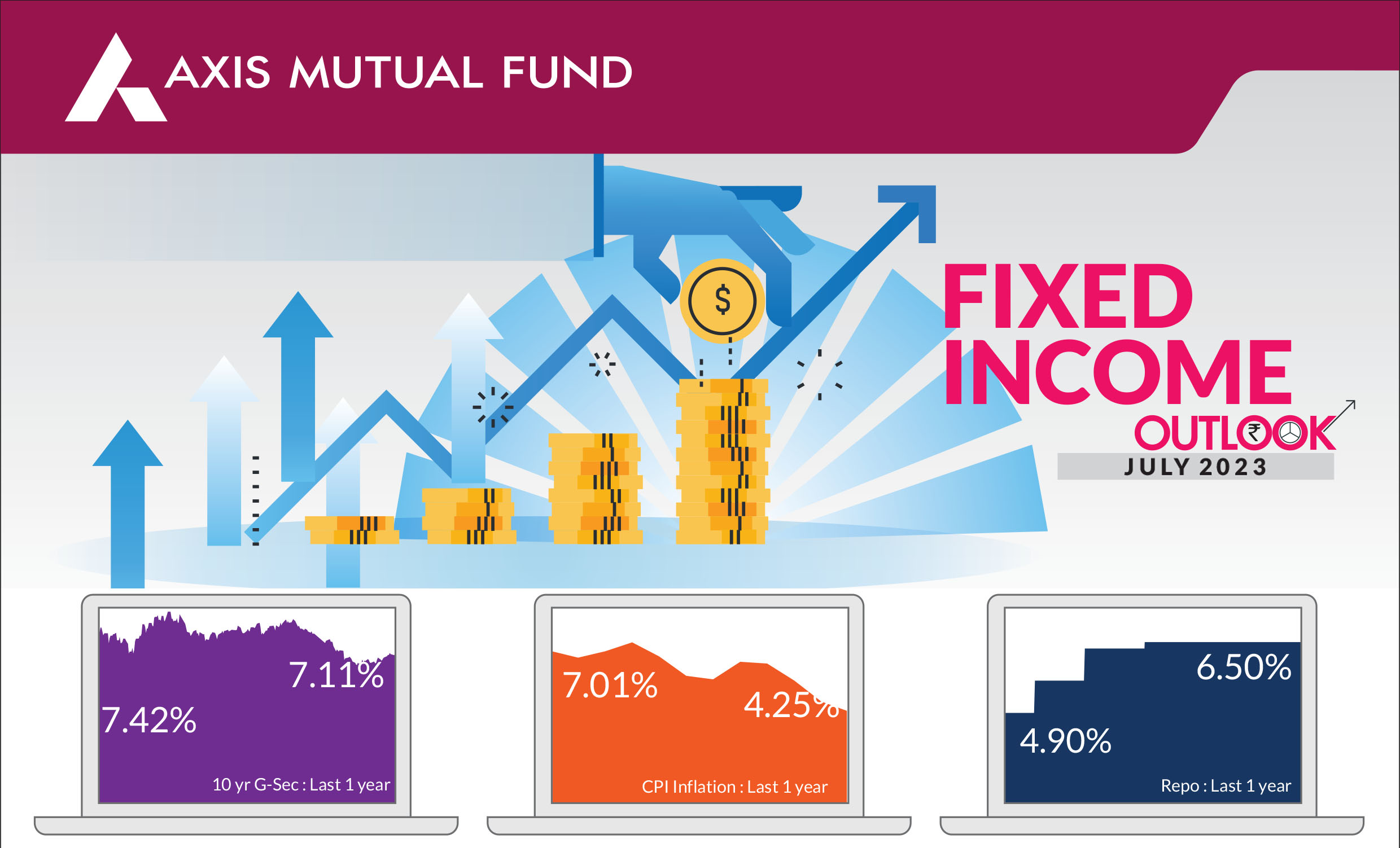

In June, the guiding theme for debt markets was the monetary policy

decisions by the Reserve Bank of India (RBI) and the central banks globally

including the US Federal Reserve (Fed). Markets also witnessed oil

production cuts by OPEC and a slew of positive macro data releases in India

and the US. All these together led to a 10-12 bps rise in yields for all bonds

over one year. Additionally, there

was a broad based rise in global

bond yields. The yield on the

benchmark 10-year G-sec stood at

7.11%, up 12 bps from last month.

The RBI's Monetary Policy

Committee (MPC) maintained a

cautious stance ahead of the US Fed's June policy meet. While the central

bank retained its status quo on interest rates, the MPC members stressed on

the 4% target for headline inflation. The US Fed policy was a consensus pause

but the policy members released Fed dot plot chart that showed two further

potential hikes while the members were upbeat on macro economy data

projections. The euphoria witnessed in the bond market since April 2023

partially reversed and currently bond yields have already priced in the

events. Markets now anticipate a long pause from the RBI and almost no rate

cuts till April 2024, and two rate hikes from Fed and no rate cuts till early

2024.

On the domestic front, as widely expected, CPI inflation declined to a 2-year

low of 4.25% in May from 4.70% a month ago. Favourable base effects and a

decline in food prices were the reason for the fall. One needs to see whether

the monsoon is deficient due to a strong El-Nino and this could push up food

prices. India's economic growth over the quarter remained resilient at 6.1%.

Meanwhile, industrial production rose 4.2% in April, up from a revised 1.7% in

March supported by investment and consumer demand. The broad-based

rise growth indicates that despite weak external demand, lower inflation and

higher capex supported industrial activity.

Headline inflation in the US cooled to its lowest in more than 2 years but core inflation still remains persistent. The Fed may find it difficult to hike rates more than once. Its emergency liquidity program to address regional bank crisis led to temporary gush of liquidity and marginal relief to weakening economic data. Good macro data and sticky inflation would mean that the Fed maintains higher interest rates for long and this could in effect add to the woes of the already weakening US economy. Recent data releases suggest ongoing weakness in the manufacturing sector although services sector remains strong. In the past nine months, markets have priced in soft landing to a recessionary scenario almost twice and this created huge volatility in global bond yields. Whilst the slowdown in economic growth has been lower than anticipated, higher rates for a longer period would eventually hurt growth. Markets are pricing in a soft landing and any data weakness would lead to global bond markets yields to rally.

Oil prices continued to trade around $70 despite a surprise production cut by OPEC to boost oil prices given weak demand. We expect weak macroeconomic outlook for China and lower commodity prices to prevail and this bodes well for inflation to remain lower globally.

In the near term, bond markets might see a marginal upside of 5-10 bps in yields. We believe investors should use this rise in yields to increase duration across their investments. Structurally, we believe we are at peak of both inflation and interest rate cycle and anticipate limited upside in yields from this point. Banking liquidity should remain positive in near term and bond prices are indicative of the supply pressures within the bond markets. Consequently, in the next 3-6 months, we expect a fall of 20-40 bps in yields across the curve beyond 1 year. We do expect the yield curve to steepen post a first rate cut by the RBI. Demand from insurance and mutual funds could decline but Rs 2,000 note deposits in banks (~ Rs 2.25 trillion already deposited) will ensure more than sufficient SLR demand from banks in near term.

From a portfolio standpoint, in line with our medium-term view, our portfolios currently run duration at the higher end of the respective investment mandates. Our expectations of incrementally softening yields across the curve and a possible policy pivot in favor of softening rates in the latter half of the financial year, this has already been factored into the current portfolio positioning. Recovery in credit spreads over the last 3-4 months has also made corporate credit (AA & above) attractive from a risk reward standpoint. For investors with a medium-term investment horizon, we continue to believe actively managed duration strategies offer ideal investment solutions to capitalize on a falling interest rate outlook and attractive 'carry' opportunities as compared to comparable traditional investment solutions.

Headline inflation in the US cooled to its lowest in more than 2 years but core inflation still remains persistent. The Fed may find it difficult to hike rates more than once. Its emergency liquidity program to address regional bank crisis led to temporary gush of liquidity and marginal relief to weakening economic data. Good macro data and sticky inflation would mean that the Fed maintains higher interest rates for long and this could in effect add to the woes of the already weakening US economy. Recent data releases suggest ongoing weakness in the manufacturing sector although services sector remains strong. In the past nine months, markets have priced in soft landing to a recessionary scenario almost twice and this created huge volatility in global bond yields. Whilst the slowdown in economic growth has been lower than anticipated, higher rates for a longer period would eventually hurt growth. Markets are pricing in a soft landing and any data weakness would lead to global bond markets yields to rally.

Oil prices continued to trade around $70 despite a surprise production cut by OPEC to boost oil prices given weak demand. We expect weak macroeconomic outlook for China and lower commodity prices to prevail and this bodes well for inflation to remain lower globally.

In the near term, bond markets might see a marginal upside of 5-10 bps in yields. We believe investors should use this rise in yields to increase duration across their investments. Structurally, we believe we are at peak of both inflation and interest rate cycle and anticipate limited upside in yields from this point. Banking liquidity should remain positive in near term and bond prices are indicative of the supply pressures within the bond markets. Consequently, in the next 3-6 months, we expect a fall of 20-40 bps in yields across the curve beyond 1 year. We do expect the yield curve to steepen post a first rate cut by the RBI. Demand from insurance and mutual funds could decline but Rs 2,000 note deposits in banks (~ Rs 2.25 trillion already deposited) will ensure more than sufficient SLR demand from banks in near term.

From a portfolio standpoint, in line with our medium-term view, our portfolios currently run duration at the higher end of the respective investment mandates. Our expectations of incrementally softening yields across the curve and a possible policy pivot in favor of softening rates in the latter half of the financial year, this has already been factored into the current portfolio positioning. Recovery in credit spreads over the last 3-4 months has also made corporate credit (AA & above) attractive from a risk reward standpoint. For investors with a medium-term investment horizon, we continue to believe actively managed duration strategies offer ideal investment solutions to capitalize on a falling interest rate outlook and attractive 'carry' opportunities as compared to comparable traditional investment solutions.

Source: Bloomberg, Axis MF Research.