► Equity market valuations are broadly reasonable adjusted for the cyclical low in earnings and

potential for revival going forward.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one's risk appetite and future goals in life.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one's risk appetite and future goals in life.

► Broadly interest rate cycles have peaked both in India and globally.

► Investors should add duration with every rise in yields.

► Mix of 10-year duration and 2-4-year duration assets are best strategies to invest in the current macro environment.

► Credits continue to remain attractive from a risk reward perspective give the improving macro fundamentals.

► Investors should add duration with every rise in yields.

► Mix of 10-year duration and 2-4-year duration assets are best strategies to invest in the current macro environment.

► Credits continue to remain attractive from a risk reward perspective give the improving macro fundamentals.

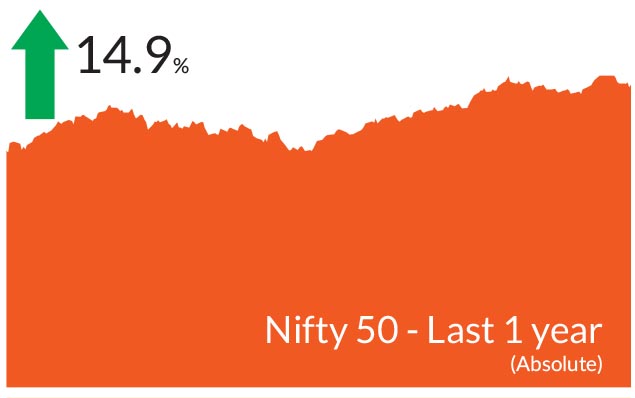

After declining in August, Indian equities regained their positive streak

of last few months on the back of better than expected macroeconomic

data, slowing inflation and inclusion of Indian government bonds in the

JP Morgan Emerging Markets Index. Key benchmark indices made

fresh lifetime highs this month; the S&P BSE Sensex gained 1.54% while

the NIFTY 50 ended 2% higher. NIFTY Midcap 100 & NIFTY Smallcap

100 continued to outperform their large-cap peers, up 3.6% and 4.1%

respectively. Market breadth remained strong with the

advance/decline ratio up over the month while volatility was lower

compared to the previous month.

► US Treasury yields rise over the month: US Treasury yields rose 45 bps over the month following concerns that the US Federal Reserve could raise interest rates once again after the pause maintained in September. Expectations of persistent inflation and higher rates for longer thereof weighed down sentiment. The potential US government shutdown on 1 October 2023 also led to worries and elevated yields. However, over the weekend, the government averted the shutdown by passing a spending bill that allows the government to stay open for 45 days giving the House and the Senate more time to finish their funding legislation.

► Inflationary pressures cool while oil prices heat up: Headline inflation moderated to 6.8% as against 7.44% seen in July due to a sharper than expected fall in vegetable prices. Core inflation, too retreated to 4.8% vs 5% in July. The measures prompted by the government earlier last month did help in tempering the prices as did the arrival of fresh stock. However, crude oil prices advanced 10% touching the $96 mark due to production cuts by Saudi Arabia and this could act as a dampener to receding inflation. Rains resumed in September and the rainfall deficit now stands at 6% in contrast to the 10% in August and as opposed to the 6% surplus of last year. However, concentrated heavy rains in some parts of India may impact the yield and the quality of kharif crops.

► Central banks screech to a halt: Central banks of the US and the UK held interest rates on pause while the European Central Bank raised rates, but all reiterated a hawkish mode and data dependency. The focus has moved from how high interest rates can go up to how long will interest rates stay elevated. Meanwhile, in the upcoming meeting on 4-6 October the Reserve Bank of India (RBI) is expected to keep interest rates on hold. The RBI has remained on a pause in the last three monetary policy meets.

Key Market Events

► India's inclusion in JP Morgan indices buoys sentiment: The news that Indian government bonds will be included in JP Morgan's Emerging market indices boosted sentiment. As per the index review, 23 bonds meet the Index eligibility criteria, with a combined notional value of approximately Rs 2.7 lakh Cr/ US$ 330 billion. As a result, India's weight is expected to reach the maximum weight threshold of 10% in the GBI-EM Global Diversified Index, and approximately 8.7% in the GBI-EM Global index. The staggered approach over the 10-month period beginning June 2024 implies an inflow of US$ 1.5 - 2 billion per month in the identified bonds. This flow is likely to boost India's profile on the world stage and further strengthen local fundamentals. Another positive outcome will be that the rupee could be more stable and the impact of rising oil prices will be moderated.► US Treasury yields rise over the month: US Treasury yields rose 45 bps over the month following concerns that the US Federal Reserve could raise interest rates once again after the pause maintained in September. Expectations of persistent inflation and higher rates for longer thereof weighed down sentiment. The potential US government shutdown on 1 October 2023 also led to worries and elevated yields. However, over the weekend, the government averted the shutdown by passing a spending bill that allows the government to stay open for 45 days giving the House and the Senate more time to finish their funding legislation.

► Inflationary pressures cool while oil prices heat up: Headline inflation moderated to 6.8% as against 7.44% seen in July due to a sharper than expected fall in vegetable prices. Core inflation, too retreated to 4.8% vs 5% in July. The measures prompted by the government earlier last month did help in tempering the prices as did the arrival of fresh stock. However, crude oil prices advanced 10% touching the $96 mark due to production cuts by Saudi Arabia and this could act as a dampener to receding inflation. Rains resumed in September and the rainfall deficit now stands at 6% in contrast to the 10% in August and as opposed to the 6% surplus of last year. However, concentrated heavy rains in some parts of India may impact the yield and the quality of kharif crops.

► Central banks screech to a halt: Central banks of the US and the UK held interest rates on pause while the European Central Bank raised rates, but all reiterated a hawkish mode and data dependency. The focus has moved from how high interest rates can go up to how long will interest rates stay elevated. Meanwhile, in the upcoming meeting on 4-6 October the Reserve Bank of India (RBI) is expected to keep interest rates on hold. The RBI has remained on a pause in the last three monetary policy meets.

Market View

Equity MarketsGoing forward, the pace of gains could moderate given the sharp rally that has led to stretched valuations across sectors. Rising crude prices coupled with higher US Treasury yields could cap the gains in the near term. The upcoming results season could likely provide fresh triggers and set the trajectory for the markets while consumption will be buoyed by the festive season. Nonetheless, India remains on a strong footing compared to its regional peers and the resilient growth outlook despite a cyclical slowdown is likely to limit downside. Markets will keenly await the outcomes of state elections later this year.

B2B growth remains strong and construction activity has become more broad-based. The upcoming elections could likely boost public capex and could result in improved demand for steel and cement. The correction seen in commodity prices could help earnings outlook for these companies. We believe that companies in the investment oriented sectors as well as select stocks in consumer discretionary could likely do well. Furthermore, given India's thrust towards manufacturing, we expect exposure to the export oriented stocks that could benefit from the China plus one theme can prove beneficial. We have been diversifying our portfolios from concentrated holdings to a broader number which has led to a wider exposure across sectors.

Markets have run up sharply in the last six months, particularly the mid and small cap segments. Our advice to our investors is to maintain a diversified approach to investing wherein risks from one asset class are balanced by the other. Furthermore, large, mid and small caps all complement each other, and rather than viewing these sectors against each other, investors should maintain their exposure to all these and keep rebalancing over a period of time. As reiterated time and again, investing through SIPs is the ideal approach to investing as the compounding effect can amplify the wealth creation potential.

Debt Markets

We believe the global slowdown is becoming more apparent and the transition from resilience to slowdown is showing though. Higher policy rates have impacted activity and this can be witnessed all the more in the US with the increasing number of corporate filings for bankruptcy, rising delinquencies on credit card loans, growing number of labour strikes and the widening fiscal deficit of the government. In addition, while the shutdown has been averted, the government faces heightened pressure. Europe through its core economy Germany is also facing moderating growth. China is definitely slowing down and while the authorities are stepping up on stimulus on the policy front and the real estate sector, the recent technical default by China's largest private property developer shows how deep the stress runs.

The central banks of the developed economies have moved towards a pause with a hawkish stance. We believe that interest rates hikes may be a thing of the past and the Fed particularly would remain on a pause for a longer period of time. While inflation has been falling globally, the rising crude oil prices make us believe "never say never" and this could be a key challenge over the short term.

In India, headline inflation declined in August but remains above RBI's comfort zone. Expectations are that it could fall further but rising crude oil prices could undermine the fall. We expect the RBI to maintain rates on hold in the policy meeting in the first week of October. Most part of the fixed income curve is pricing in no cuts for the next one year. As reiterated earlier, we do believe that interest rates have peaked globally as well as in India and probability of further hikes are limited. With policy rates remaining incrementally stable, we have added duration gradually across our portfolios within the respective scheme mandates. We do expect the 10-year bond yields to touch 6.75% by April - June 2024.

From a strategy perspective, we have added duration across portfolios within the respective investment mandates. We expect our duration call to add value in the medium term. Investors could use this opportunity to top up on duration products with a structural allocation to short and medium duration funds and a tactical play on GILT funds.

Source: Bloomberg, Axis MF Research.