► Equity market valuations are broadly reasonable adjusted for the cyclical low in earnings and

potential for revival going forward.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one's risk appetite and future goals in life.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one's risk appetite and future goals in life.

► Broadly interest rate cycle and inflation cycle have peaked both in India and globally.

► Investors should add duration with every rise in yields.

► Mix of 10-year duration and 2-4-year duration assets are best strategies to invest in the current macro environment.

► Credits continue to remain attractive from a risk reward perspective give the improving macro fundamentals.

► Investors should add duration with every rise in yields.

► Mix of 10-year duration and 2-4-year duration assets are best strategies to invest in the current macro environment.

► Credits continue to remain attractive from a risk reward perspective give the improving macro fundamentals.

Following four months of consistent positive returns, Indian equities

retreated on the back of relatively weak FPI flows and higher yields on

US Treasuries. In addition, the downgrade of US credit rating from AAA

to AA+ by Fitch, higher oil prices, slowing demand in China and a weak

monsoon dampened investor sentiment. After hitting lifetime highs in

July, benchmark indices witnessed profit booking and during the entire

month, benchmark indices remained in a sideways to negative zone.

Both S&P BSE Sensex & NIFTY 50 ended the month down 2.5% each. In

contrast, NIFTY Midcap 100 & NIFTY Smallcap 100 continued to

outperform their large-cap peers, up 3.7% and 4.6% respectively.

Market breadth remained strong with the advance/decline ratio up

over the month while volatility was up compared to the previous month.

► Inflationary pressures may cool down: Headline inflation surprised with a print of 7.44% vs a revised 4.9% in June due to a sharp rise in vegetable prices. Core inflation, on the other hand, moderated to 5% in July from 5.2% in June. On a positive note, food inflation is expected to subside with the arrival of fresh stock and government measures to bring down tomato prices. The government banned non-basmati rice exports and levied a 40% tax on onion exports to tame inflation. In addition, the government lowered cooking gas prices by Rs 200 a cylinder which will be favourable. The key risks are a second round impact of spike in food inflation and deficient rains. El-Nino impact in August has led to a cumulative rainfall deficiency at 8% below normal and almost 39-40% of India's districts have received scarce rains.

► RBI reins in liquidity through temporary measures: The minutes of RBI's monetary policy meeting suggest that the central bank is not overly concerned about volatility in inflation but will be quick footed to address any second round impact on core inflation. Earlier in the month, in its monetary policy meeting, the Reserve Bank of India (RBI) maintained a hawkish pause on interest rates but brought in a surprise CRR action of 10% on incremental deposits made between May 19 and July 28, 2023 and committed to review the action on or before 8 September 2023. The excess liquidity gave way to an orchestrated deficit since the measure and yields witnessed a rise more over the shorter end of the yield curve. We expect the advance tax collections in this month and the festive season to further add to the deficit. The minutes of the RBI's monetary policy meeting reiterated focus on price stability, anchoring inflationary expectations and achieving the 4% target over the medium term.

► Higher growth momentum: India remained the fastest growing economy with GDP accelerating 7.8% in Q1FY24 vs 6.1% in Q4FY24 and just a tad below RBI's projection of 8%. Investment growth outpaced consumption and services sector maintained a strong momentum led by financial services while exports was a drag. Going forward, the growth momentum could likely weaken due to softer consumption, albeit. The festive season may lend some cheer. A sustained capex recovery, healthy corporate and bank balance sheets, and governments pend ahead of state /central elections could support growth.

Key Market Events

► US Treasury yields rise over the month: A slew of factors such as (a) increased debt issuance from $733 billion to $1 trillion over the July- September period, (b) a higher fiscal deficit and (c) expectations of elevated interest rates in light of a relative stronger macroeconomic scenario led to a surge in bond yields. The 10-year Treasury saw yields rising to highs of 4.34% over the period before cooling off to end at 4.11%. A significant event that did not have much of an impact was the downgrade of long term debt from AAA to AA+. Incoming data has been pointing to a softening scenario, however jobs data suggested an addition to jobs but a high unemployment rate at the same time.► Inflationary pressures may cool down: Headline inflation surprised with a print of 7.44% vs a revised 4.9% in June due to a sharp rise in vegetable prices. Core inflation, on the other hand, moderated to 5% in July from 5.2% in June. On a positive note, food inflation is expected to subside with the arrival of fresh stock and government measures to bring down tomato prices. The government banned non-basmati rice exports and levied a 40% tax on onion exports to tame inflation. In addition, the government lowered cooking gas prices by Rs 200 a cylinder which will be favourable. The key risks are a second round impact of spike in food inflation and deficient rains. El-Nino impact in August has led to a cumulative rainfall deficiency at 8% below normal and almost 39-40% of India's districts have received scarce rains.

► RBI reins in liquidity through temporary measures: The minutes of RBI's monetary policy meeting suggest that the central bank is not overly concerned about volatility in inflation but will be quick footed to address any second round impact on core inflation. Earlier in the month, in its monetary policy meeting, the Reserve Bank of India (RBI) maintained a hawkish pause on interest rates but brought in a surprise CRR action of 10% on incremental deposits made between May 19 and July 28, 2023 and committed to review the action on or before 8 September 2023. The excess liquidity gave way to an orchestrated deficit since the measure and yields witnessed a rise more over the shorter end of the yield curve. We expect the advance tax collections in this month and the festive season to further add to the deficit. The minutes of the RBI's monetary policy meeting reiterated focus on price stability, anchoring inflationary expectations and achieving the 4% target over the medium term.

► Higher growth momentum: India remained the fastest growing economy with GDP accelerating 7.8% in Q1FY24 vs 6.1% in Q4FY24 and just a tad below RBI's projection of 8%. Investment growth outpaced consumption and services sector maintained a strong momentum led by financial services while exports was a drag. Going forward, the growth momentum could likely weaken due to softer consumption, albeit. The festive season may lend some cheer. A sustained capex recovery, healthy corporate and bank balance sheets, and governments pend ahead of state /central elections could support growth.

Market View

Equity MarketsThe Q1FY24 results season ended on a strong note. Consumer demand was robust as represented by performance across the auto and financial sectors. The auto sector benefited from weaker raw material prices in addition to strong demand in the build-up to the festive season. Likewise, state-run banks and small banks showed impressive category-specific results. Earnings momentum was also supported by the hospitality and travel sector. IT, cement, chemicals, and metals faced headwinds due to weaker realizations, higher costs and global demand constraints.

Going forward, the sharp outperformance of the mid and small-cap sectors and the rich valuations across sectors could cap gains. The gains in the last few months have rendered valuations expensive v/s regional peers. However, India's strong macroeconomic position, improving profitability and volumes in the consumption sectors, and the resilient growth narrative are likely to limit downside. The key drivers for markets in the next few months will be the festive season-led recovery and the state elections later this year.

Over the last year, we have diversified our portfolios from concentrated holdings to a broader number which has led to a wider exposure across sectors. The rationale being that the market offers lot more opportunities more so in niche holdings. For instance, in the capital goods and power sectors, we prefer niche names than the traditional ones. This is where active stock selection comes into play.

Given that markets have seen a strong run in the last few months, we suggest investors should maintain a diversified approach to investing wherein risks from one asset class are balanced by the other. Furthermore, large, mid and small caps all complement each other, and rather than viewing these sectors against each other, investors should maintain their exposure to all these and keep rebalancing over a period of time.

Debt Markets

Headline inflation is sharply above RBI's comfort zone. However, these levels seem transient and we believe that the RBI would be watchful but not as concerned. CPI should cool off soon and we can already see a drop in vegetable prices as a result of the measures taken by the government. Meanwhile, a truant monsoon could play spoilsport; August had a deficit after the surplus in July.

The minutes of the Fed meeting indicate that the central bank could perhaps hike interest rates one last time. Major indicators are pointing to a softening bias and inflationary pressures too seem to be subdued. The increasing mortgage rates, higher bankruptcies and credit card defaults could fuel the slowdown. Right now, it's a wait and watch approach and we reiterate our earlier view that we do not see rate cuts before the first quarter of 2024.

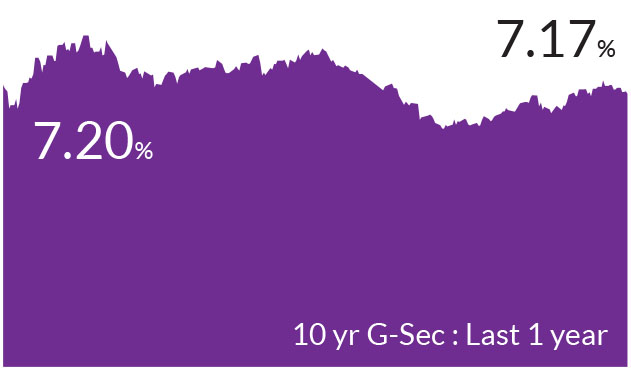

Most part of the fixed income curve is pricing in no cuts for the next one year. We believe that we are at peak of interest rate cycles, globally as well as in India and probability of further hikes are limited. Policy actions and commentary are in line with our view. We retain our thesis of peak rates within the current market environment. With policy rates remaining incrementally stable, we have added duration gradually across our portfolios within the respective scheme mandates.

We do expect the 10-year bond yields to touch 6.75% by April - June 2024. Investors should use the uptick in yields to increase duration and should stick to short to medium term funds with tactical allocation to long / dynamic bond funds in this macro environment. One can expect yields to be lower by 25-40 bps in next 6-12 months across the curve. Investors can look at actively managed strategies to capitalize from fluctuations in rate movements. While the overall strategy is to play flat/falling interest rate cycle over the next 18-24 months, markets are likely to see sporadic rate movements. In such a scenario, active funds are ideally positioned to toggle across duration and the ratings curve to optimize medium term returns.

Source: Bloomberg, Axis MF Research.