► Markets do remain overvalued across the investment part of the economy and we may see

normalisation in some of these segments.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one's risk appetite and future goals in life.

► We remain bullish on equities from a medium to long term perspective.

► Investors are suggested to have their asset allocation plan based on one's risk appetite and future goals in life.

► Expect lower interest rates in the second half of FY25.

► Investors should add duration with every rise in yields, as yield upside limited.

► Mix of 10-year maturity and 1-2-year maturity assets are best strategies to invest in the current macro environment.

► Selective Credits continue to remain attractive from a risk reward perspective given the improving macro funda mentals.

► Investors should add duration with every rise in yields, as yield upside limited.

► Mix of 10-year maturity and 1-2-year maturity assets are best strategies to invest in the current macro environment.

► Selective Credits continue to remain attractive from a risk reward perspective given the improving macro funda mentals.

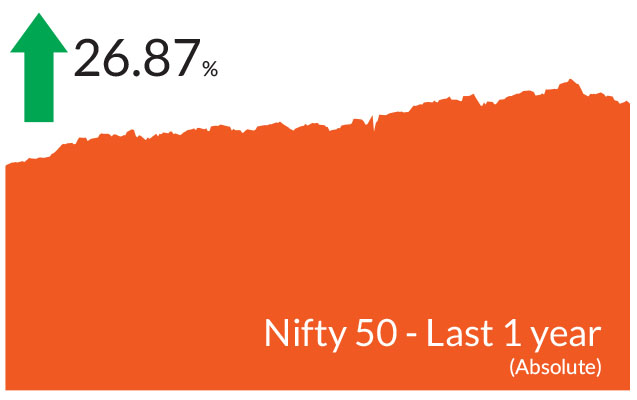

Indian equites ended October lower in a month marked by volatility.

Globally, equities were impacted for many reasons - geopolitical

conflicts between Iran and Israel, stimulus measures by China, rising

crude oil and commodity prices and the uncertainty regarding the

upcoming presidential elections in the US. India too was impacted by

global developments. In addition, weaker than expected second

quarter results, elevated valuations and foreign fund outlows resulted

in markets retreating from all-time highs. To set the context, NSE 500

saw 175 stocks fall 25% from their highs in October while benchmark

indices witnessed a fall of 8-10% from their lifetime highs seen in

September. The BSE Sensex and the NIFTY 50 ended the month lower

by 5.8% and 6.2% respectively. The NIFTY Midcap 100 ended the

month lower 6.7% while NIFTY Small Cap 100 ended 3.2% lower and

outperformed both large and mid caps.

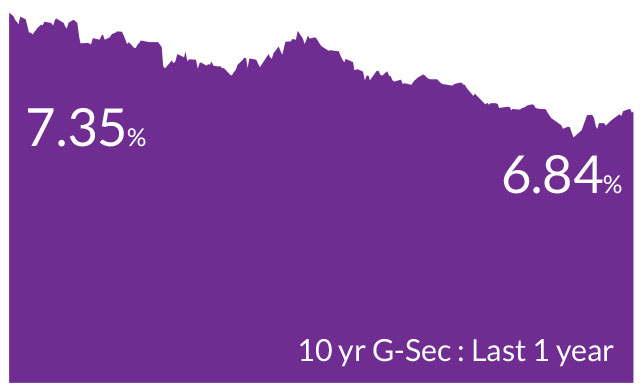

The highlight of the month was change in monetary policy stance by the Reserve bank of India's (RBI) monetary policy committee. Comfort on inflation trajectory, Fed cut of 50 bps and good monsoon helped the central bank to overlook near term uptick in inflation and change the monetary policy stance. Overall, bond markets yields both in India and US witnessed an uptick in the last 30 days; US 10 year yields were up 50 bps and Indian 10 year yields up by 10 bps from the last month. Foreign Portfolio Investors (FPI) withdrew to the tune of US$0.4 bn over the month. Year to date, cumulative debt inflows amounted to US$16.8bn.

► Inflationary pressures rise : Headline inflation reached 5.49%, surpassing market expectations due to base effects and rising vegetable prices. We anticipate the October figure to also be on the higher side, around 5.75%. However, we expect headline CPI to return to the 4.5% range after November and do not foresee any changes in the full-year CPI projections.

► Banking liquidity in surplus : Banking liquidity has remained in surplus, supported by government buybacks and slower credit growth, which have helped stabilize money market yields. The year-to-date incremental credit-deposit ratio is below 60%, and we believe banking liquidity will remain comfortable for this quarter.

The highlight of the month was change in monetary policy stance by the Reserve bank of India's (RBI) monetary policy committee. Comfort on inflation trajectory, Fed cut of 50 bps and good monsoon helped the central bank to overlook near term uptick in inflation and change the monetary policy stance. Overall, bond markets yields both in India and US witnessed an uptick in the last 30 days; US 10 year yields were up 50 bps and Indian 10 year yields up by 10 bps from the last month. Foreign Portfolio Investors (FPI) withdrew to the tune of US$0.4 bn over the month. Year to date, cumulative debt inflows amounted to US$16.8bn.

Key Market Events

►Higher yields across economies : The Reserve Bank of India (RBI) retained a pause on interest rates for the tenth consecutive time; but changed its stance from 'withdrawal of accommodation' to 'neutral'. Expectations are for lower interest rates across the US, UK and Europe over the next few months. Despite the rate cuts, yields rose over the month. One of the main reasons for the rise in US Treasury yields has been the growing likelihood of Donald Trump getting elected as the US President. This could result in a higher US fiscal deficit and increased near-term inflation due to tariffs, tax cuts, and potential delays in Federal Reserve (Fed) rate cuts. Another reason for uptick in yields has been China's stimulus package of RMB 4 trillion (approximately $586 billion) to boost its economy also led to uptick in crude and other commodities and also in yields.► Inflationary pressures rise : Headline inflation reached 5.49%, surpassing market expectations due to base effects and rising vegetable prices. We anticipate the October figure to also be on the higher side, around 5.75%. However, we expect headline CPI to return to the 4.5% range after November and do not foresee any changes in the full-year CPI projections.

► Banking liquidity in surplus : Banking liquidity has remained in surplus, supported by government buybacks and slower credit growth, which have helped stabilize money market yields. The year-to-date incremental credit-deposit ratio is below 60%, and we believe banking liquidity will remain comfortable for this quarter.

Market View

Equity MarketsThe second quarter earnings season has been weak so far and in line with expectations of slowing underlying growth. Companies have broadly disappointed across sectors. Consumer companies reported weak prints so far, with suggestive of a challenging demand environment. Demand has been subdued for the urban market, while rural growth contributed positively to overall growth. IT companies reported healthy performance but outlook remains somewhat cautious. Banks have done reasonably well, with moderate credit growth, stable NIMs and asset quality. Automobiles saw results aligned with expectations, mainly driven by domestic two wheeler volume growth and a sequential recovery in exports. Within consumers, results so far have been slightly lower than expected. Earnings growth for pharma companies remained healthy particularly for the domestic formulation business.

Looking ahead, slowing global growth, interest rate cuts in India, the outcome of US presidential elections and geopolitical stress are the events to look out for. Given the 8-10% fall from record highs, Indian indices are now at relatively attractive valuations. Particularly in the large cap segment, valuation concerns have been declining, and concerns have shifted towards earnings growth. Our advice to our investors is to view any declines and volatility to increase exposure to equities and stay invested based on investor goals, investment horizon and risk profile with a long-term view.

Overall, against the slowing global backdrop, India maintains its position as one of the fastest growing economies globally. Macros remain strong with an easing inflation cycle, good monsoons and robust economic growth. At a sector level, we remain positive on our themes of being overweight consumption, manufacturing, infrastructure and being underweight exports. Overall, we have reduced our overweight in automobiles and increased exposure to pharmaceuticals and banks. We maintain an overweight in capital goods and within this segment, we believe power will be a sustainable theme followed by defence.

As the festive season wraps up, we will see its impact on consumption in a few weeks when the monthly high-frequency indicators are released. Overall, we believe that India's consumption story is fundamentally strong. The housing sector has seen increased absorption across India, and with the government's emphasis on affordable housing, building materials and related industries are poised to benefit. Separately, multiple enablers such as deleveraged corporate balance sheets, healthy profitability, rising domestic demand, and increasing capacity utilization bodes well for the capex cycle.

Debt Markets

At the current juncture, it is interesting to note that yields are up despite the Fed rate cut, change in stance by the RBI and easy banking liquidity. As already mentioned earlier, yields are higher due to a higher probability of Trump getting elected. Nevertheless, even if Trump is elected as the president, the economy is slowing own and the current macro environment makes us believe the Fed could deliver 50 bps cut this year and 100 bps cut next year. US Treasury futures are not currently pricing in aggressive rate cuts. As such, we believe the sell-off in US yields is largely overdone and expect US Treasury yields to soften.

Separately, though, the measures announced by the Chinese government are of significant magnitude It is too early to conclude their execution and impact on global macros, inflation, and commodities.

In India, we believe that the change of stance, the RBI has already pivoted. As India's growth remains strong, we do not expect the RBI to be aggressive in cutting rates and expect 50 bps of rate cuts in next 6 months. We believe that banking liquidity would continue to remain positive in this quarter and expect money market yields to remain stable. Due to favourable demand supply dynamics, we continue to have a higher bias towards government bonds.

Source: Bloomberg, Axis MF Research.